How I Protected My Future When Love Came Knocking the Second Time

What happens when love finds you again, but your finances aren’t ready? I’ve been there—excited about a new chapter, only to realize the risks hiding beneath the surface. Blending lives means blending money, and without clear planning, even the strongest relationships can face strain. This is not just about love; it’s about protection, clarity, and smart moves that safeguard what you’ve built—without sounding cold or untrusting. Many people entering second marriages focus on emotional healing and companionship, which is natural and important. But behind the joy lies a network of financial responsibilities that, if ignored, can unravel years of hard-earned stability. The truth is, second marriages often carry more complex financial dynamics than first ones, especially when children, inheritances, and retirement plans are involved. With the right approach, however, love and financial security don’t have to be at odds.

The Emotional Crossroads: When Love Meets Finances

Remarrying later in life brings a unique blend of hope, companionship, and emotional renewal. For many, it’s a second chance at happiness after loss or divorce. Yet, this new beginning often arrives with financial histories that don’t simply vanish with a wedding ring. Unlike first marriages, where couples typically start with limited assets and shared goals, second marriages frequently involve established careers, accumulated savings, homes, and sometimes, children from previous relationships. These factors create a more intricate financial landscape that demands thoughtful navigation.

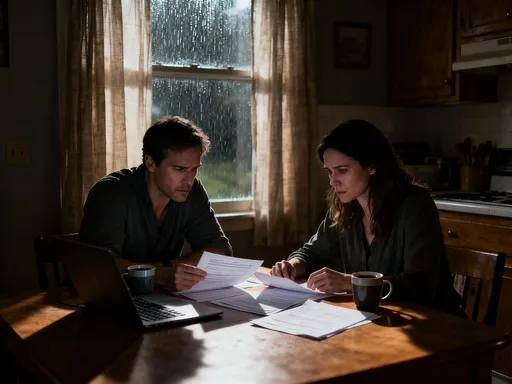

Consider the case of a woman in her early 50s who reconnected with an old friend after her divorce. They fell in love quickly, moved in together, and planned to marry within a year. Excited by their renewed romance, they merged bank accounts and began making joint purchases—furniture, vacations, even a car. But when her partner unexpectedly lost his job, the financial strain exposed deeper issues. His past credit card debt, which he had not fully disclosed, began affecting their shared credit. What started as a gesture of trust became a source of tension and resentment. This scenario is not uncommon. Emotional momentum often outpaces financial due diligence, especially when people are eager to avoid conflict or appear overly cautious.

The challenge lies in balancing emotional openness with financial prudence. Many believe that discussing money before marriage signals a lack of trust, but the opposite is true. Transparent conversations about finances are among the most trusting things a couple can do. They lay the foundation for mutual respect and long-term stability. Without them, even the most loving relationships can stumble under the weight of unspoken expectations and mismatched financial habits. The key is to approach these discussions not as interrogations, but as collaborative planning—just as couples plan their wedding or future home, they should plan their financial life together.

Moreover, societal norms often fail to address the financial complexities of remarriage. Traditional financial advice tends to focus on young couples building wealth, not on midlife partners protecting what they’ve already achieved. This gap leaves many feeling unprepared. They may not realize that legal rights automatically shift upon marriage—rights that can override prior estate plans or individual financial decisions. Therefore, understanding the financial implications of remarriage isn’t about pessimism; it’s about empowerment. It allows individuals to enter a new relationship with eyes wide open, ready to build something lasting without sacrificing their hard-earned security.

Hidden Risks in Blending Families and Finances

When two people remarry, especially later in life, they’re not just merging two lives—they’re often merging two families, each with its own financial needs and expectations. This blending can introduce subtle but significant risks that go far beyond shared household expenses. One of the most common yet overlooked issues is the financial responsibility toward children from previous relationships. While love may be unconditional, financial obligations are not. In many cases, stepparents feel a natural desire to support their partner’s children, whether through education funding, daily expenses, or future inheritances. However, without clear agreements, these well-intentioned acts can lead to resentment or financial imbalance.

Take, for example, a man who remarried and wanted to help pay for his stepdaughter’s college tuition. He believed this was a fair gesture of support and inclusion. However, he hadn’t discussed it with his adult biological children, who later felt their inheritance was being diluted. This created family tension and complicated estate planning. The issue wasn’t generosity—it was the lack of advance communication and documentation. Financial decisions made in the spirit of unity can unintentionally create inequities, especially when children from prior relationships are involved. Without clarity, assumptions fill the silence, and those assumptions can damage relationships over time.

Another hidden risk lies in housing and property decisions. When a couple combines households, one partner may sell their home to move in with the other. On the surface, this seems practical. But what happens if the relationship ends? The partner who gave up their home may have no place to return to and may have lost years of home equity growth. Even in long-term remarriages, this can be problematic if the surviving spouse is not legally entitled to remain in the home after the other’s passing. Joint ownership seems like a solution, but it comes with its own complications—such as tax implications, liability exposure, and the potential for disputes among heirs.

Additionally, retirement planning becomes more complex when supporting multiple generations. A woman in her 60s may be helping her adult child with a mortgage while also saving for her own retirement and planning for long-term care. When she remarries, her new spouse may have different financial priorities—perhaps he wants to travel or downsize. Without a shared financial plan that accounts for all these responsibilities, conflicts arise. The solution is not to avoid generosity or family support, but to structure it intentionally. This means defining financial roles, setting limits, and documenting expectations in a way that respects everyone’s needs without creating hidden burdens.

Pre-Marital Financial Clarity: More Than Just a Prenup

When people hear the word “prenup,” they often think of celebrity divorces or cold, transactional relationships. But for those entering a second marriage, a prenuptial agreement is less about preparing for failure and more about ensuring fairness and clarity. It’s a tool that allows both partners to enter the marriage with a clear understanding of what belongs to whom and how assets will be handled in various scenarios. However, a prenup is just one part of a broader strategy for financial transparency before remarriage.

Many couples benefit from creating a comprehensive financial disclosure before marriage. This includes listing all assets, debts, income sources, and future financial obligations. While this may feel intrusive, it’s no different than sharing medical history before a serious commitment. Full disclosure builds trust and prevents surprises later. Some couples also choose to keep certain assets separate, such as a home inherited from a first spouse or retirement funds accumulated before the relationship. This doesn’t mean withholding love or support—it means protecting individual legacies while building a shared future.

For those who marry without a prenup, a postnuptial agreement can serve a similar purpose. It’s a legally binding document created after the wedding that outlines how assets and debts will be handled. While less common, it’s a valuable option for couples who didn’t plan ahead but now recognize the need for clarity. Additionally, establishing separate bank accounts for pre-marriage assets, while maintaining a joint account for shared expenses, can provide both independence and unity. This structure allows each partner to maintain financial autonomy while contributing fairly to household costs.

Having these conversations doesn’t have to be awkward. The key is to frame them as part of responsible planning, not as a sign of distrust. Couples can work with a financial advisor or attorney to guide the discussion in a neutral, professional setting. The goal is not to plan for divorce, but to ensure that both partners feel secure and respected. When financial expectations are aligned from the start, the relationship is free to grow on a foundation of honesty and mutual understanding.

Protecting Legacy: Assets, Inheritance, and Children from Prior Relationships

One of the most pressing concerns for individuals in second marriages is ensuring that their children from prior relationships are not unintentionally disinherited. State laws often give surviving spouses automatic rights to a portion of an estate, which can override even the most carefully written will. For example, in many jurisdictions, a surviving spouse is entitled to at least one-third to one-half of the deceased’s assets, regardless of what the will says. This means that a parent who intends to leave everything to their children could inadvertently leave a significant portion to their new spouse, creating family conflict.

To protect children’s inheritance, estate planning becomes essential. A properly drafted will is the starting point, but it’s not always enough. Trusts offer a more powerful solution. A revocable living trust, for instance, allows a person to outline exactly how their assets should be distributed after death. It can specify that certain assets go directly to children while providing the surviving spouse with income or use of a home during their lifetime. This approach balances care for the current spouse with long-term protection for biological or adopted children.

Another critical step is reviewing and updating beneficiary designations on retirement accounts, life insurance policies, and bank accounts. These designations often override wills, meaning that even if a will leaves everything to children, a retirement account with a spouse named as beneficiary will go directly to the spouse. Many people forget to update these forms after a divorce or remarriage, leading to unintended outcomes. Taking time to review all accounts ensures that intentions match reality.

Additionally, clear communication with adult children is vital. While parents are not obligated to share every detail, having open conversations about estate plans can prevent misunderstandings later. Explaining the reasoning behind decisions—such as providing for a new spouse during their lifetime—can help children feel respected and included. The goal is not to eliminate all conflict, but to reduce the likelihood of resentment and legal disputes. With thoughtful planning, it’s possible to honor both love and legacy.

Debt Transparency: The Silent Relationship Killer

Debt is often the most sensitive and least discussed topic in relationships, yet it can have the greatest impact on financial harmony. In second marriages, where individuals may carry debt from previous relationships or life events, the stakes are even higher. Unresolved debt—whether from credit cards, medical bills, or past loans—can quickly become a shared burden, especially in community property states where debts incurred during marriage are considered joint liabilities.

Even in non-community property states, financial entanglement can occur. For example, if one partner has poor credit due to past debt, it can affect the couple’s ability to secure a mortgage, refinance a home, or qualify for favorable interest rates. This doesn’t mean someone with debt should be judged or excluded, but it does mean that both partners need a realistic understanding of the situation. Hiding debt, even out of shame or fear, undermines trust and can lead to financial strain down the road.

The solution begins with full disclosure. Each partner should share a complete picture of their financial obligations, including monthly payments, interest rates, and repayment timelines. This isn’t about assigning blame—it’s about creating a shared understanding. From there, couples can develop a plan to manage debt responsibly. This might include setting up a repayment schedule, consolidating high-interest debt, or agreeing that certain debts will remain the individual responsibility of the person who incurred them.

It’s also important to establish boundaries. For example, a couple might agree that new joint debt will only be taken on for shared goals, like home improvements, while existing personal debt remains separate. This protects both partners and ensures that one person’s financial past doesn’t unfairly impact the other’s future. Open, ongoing conversations about debt reduce stress and foster cooperation, turning a potential source of conflict into an opportunity for teamwork.

Retirement Realities: Merging Plans Without Losing Security

Retirement accounts are often among the most valuable assets a person owns, especially after decades of saving. When entering a second marriage, decisions about these accounts become both personal and financial. By law, most retirement plans, including 401(k)s and IRAs, require the spouse to be the primary beneficiary unless a waiver is signed. This means that even if someone intends to leave their retirement savings to their children, the current spouse may automatically inherit the funds unless proper documentation is in place.

This legal reality can create tension, especially if the spouse is much younger or if the account holder wants to preserve wealth for their children. The key is to plan ahead. One option is to designate a trust as the beneficiary of the retirement account, with specific instructions for how the funds should be distributed. Another approach is to balance inheritances by leaving other assets—such as life insurance proceeds or real estate—to children, while naming the spouse as the beneficiary of retirement accounts.

Social Security benefits also require careful consideration. A remarried person may be eligible for benefits based on their new spouse’s work record, but only if the marriage lasts at least 10 years. Additionally, if a person was married for 10 or more years in a previous marriage, they may still qualify for benefits based on that ex-spouse’s record, provided they haven’t remarried before age 60. These rules are complex, and understanding them can help couples make informed decisions about when to claim benefits and how to maximize household income in retirement.

The goal is not to exclude anyone, but to ensure that all parties are provided for in a way that reflects the couple’s values and intentions. Working with a financial advisor who specializes in retirement and estate planning can help navigate these decisions with clarity and confidence.

Building a Shared Future—Safely

While much of this discussion has focused on protection and risk, the ultimate goal is not to build walls, but to build a stronger, more resilient partnership. Financial clarity doesn’t diminish love—it enhances it. When couples approach money with honesty and structure, they reduce stress, avoid misunderstandings, and create space for deeper connection. The most successful second marriages are not those where finances are perfectly equal, but where both partners feel heard, respected, and secure.

One practical way to achieve this is by creating a joint budget that includes defined contribution rules. For example, each partner might agree to contribute a percentage of their income to shared expenses, while maintaining separate accounts for personal spending. This model supports fairness without requiring complete financial merger. It also allows each person to maintain a sense of autonomy, which is especially important for those who have worked hard to regain financial independence after a previous divorce or loss.

For families with complex dynamics, establishing a family council can be helpful. This doesn’t need to be formal—just a regular time when key financial decisions are discussed with input from adult children or other stakeholders. It fosters transparency and inclusion, reducing the chance of surprises or conflicts later. Topics might include major purchases, estate planning updates, or long-term care decisions.

Ultimately, remarriage offers a second chance—not just for love, but for wiser choices. The lessons learned from past experiences can guide more thoughtful financial decisions today. By combining emotional openness with practical planning, couples can create a future that honors both the heart and the hard work of the past. True security comes not from secrecy, but from shared clarity. And in that clarity, love can thrive.

Remarriage doesn’t have to mean financial compromise. With thoughtful planning, it’s possible to honor both love and legacy—protecting the past while embracing the future. The smartest move isn’t avoiding emotion, but channeling it into structure. Because true security comes not from keeping secrets, but from sharing clarity.